A collection notice can make an ordinary Tuesday feel like a legal emergency. The phone rings, the letter looks official, and suddenly you are trying to decide whether to pay, argue, ignore it, or panic. Debt collection rights exist because Americans should not have to guess their way through pressure, threats, or confusing claims about old bills. In the United States, collectors have rules to follow, and you have more power than most people realize.

The mistake many people make is thinking the collector controls the whole conversation. They do not. You can slow the process down, ask for proof, protect your credit, and push back when a company crosses the line. Sites that publish plain-language financial protection resources help readers understand these issues before stress turns into a rushed decision.

The goal is not to dodge money you truly owe. The goal is to stop fear from making choices for you. A fair system starts when you know where the lines are.

How Debt Collectors Must Treat You Under U.S. Law

Debt collection is not a free-for-all, even when the bill is real. Federal law places limits on how third-party collectors can contact you, what they can say, and how much pressure they can apply. The hard part is that many people never learn those limits until a collector has already pushed them into a corner.

Why Fair Debt Collection Starts With Clear Boundaries

Fair debt collection depends on one basic idea: a collector may ask for payment, but they cannot bully you into it. That difference matters. A legitimate call should identify the company, explain the debt, and give you room to respond without threats or tricks.

A collector cannot pretend to be law enforcement, claim you will be arrested for ordinary consumer debt, or use abusive language to scare you. They also cannot call at odd hours that fall outside legal limits. If a collector calls before sunrise or late at night, that is not persistence. That is pressure dressed up as business.

One common example happens when a person falls behind on a medical bill after an insurance denial. The collector may call often and speak as if payment is the only option. In reality, you can ask for details, check the original provider’s billing records, and dispute errors before paying a cent.

What Collection Agency Rules Mean During Contact

Collection agency rules also shape how collectors communicate with your family, workplace, and employer. In most cases, collectors cannot discuss your debt with relatives, neighbors, or coworkers. They may try to locate you, but they cannot turn your private financial stress into public embarrassment.

Work calls deserve extra attention. If you tell a collector that your employer does not allow personal calls, the collector must stop contacting you there. That one sentence can protect your job from unnecessary drama. Write down when you said it, who you spoke with, and what happened after.

Text messages and emails have added another layer. A collector may reach out through newer channels, but that does not give them permission to flood your phone or hide required information. The medium changed. The rules did not disappear.

Using Debt Collection Rights Before You Pay Anything

The first move should rarely be payment. That sounds odd, especially when the letter demands money and warns about consequences. Yet smart consumer debt protection starts with verification, because collection accounts are often sold, transferred, mixed up, or updated badly.

How to Ask for Debt Validation Without Sounding Defensive

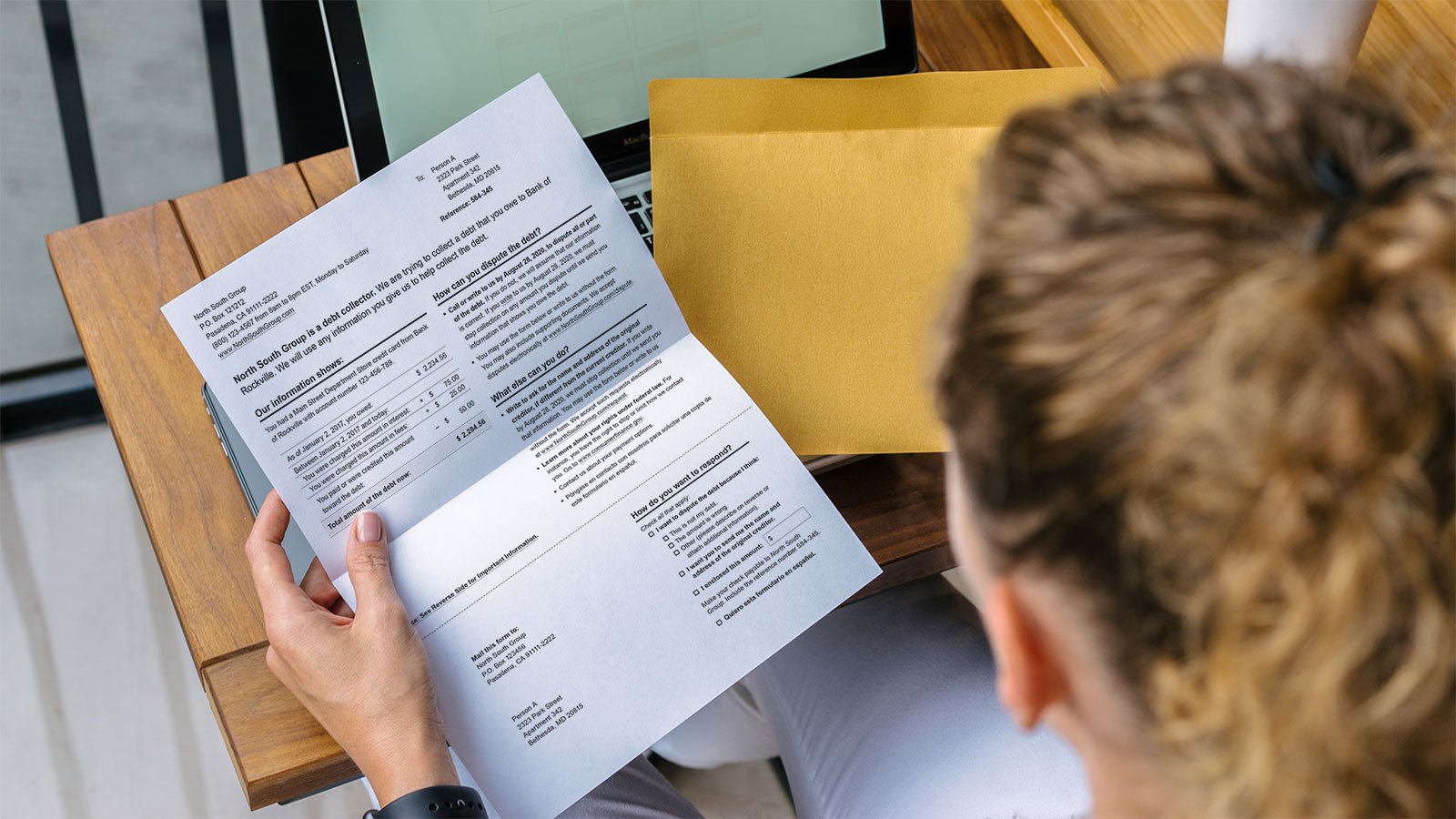

A validation request asks the collector to prove the debt is yours and that they have the right to collect it. This is not rude. It is basic financial hygiene. You would not pay a random invoice from a company you do not recognize, so you should not pay a collection claim without proof.

Your request should be simple. Ask for the original creditor’s name, the amount claimed, the account details, and documentation showing the collector’s authority. Keep a copy of the letter or email. If you send it by mail, use a method that confirms delivery.

A counterintuitive truth: a calm written request often works better than an angry phone call. Phone calls create heat. Paper creates a record. A collector who knows you are documenting the exchange may act with more care.

Why Consumer Debt Protection Depends on Timing

Consumer debt protection works best when you respond early. Waiting does not always destroy your options, but it can make the mess harder to untangle. A collector may continue reporting the account, the debt may move to another agency, or a lawsuit may arrive before you have built your paper trail.

Timing also matters because old debts can be legally complicated. Some debts may be too old for a collector to sue over, depending on your state and the type of account. That does not always erase the debt, but it may change what a collector can legally do.

This is where many Americans get trapped. They make a tiny payment on an old account because the collector sounds friendly. In some states, that payment may affect the legal clock. Before paying an old debt, slow down and check your state’s rules or speak with a qualified consumer attorney.

Protecting Your Credit When a Collection Account Appears

A collection account can hurt more than your monthly budget. It can affect loan approvals, apartment applications, insurance pricing in some states, and even your confidence when making normal financial choices. The credit side of collection is often where quiet damage happens.

How Credit Report Disputes Can Fix Wrong Information

Credit report disputes give you a way to challenge information that is false, incomplete, outdated, or unverifiable. Start by checking all three major credit reports, because one bureau may show a collection account that another does not. Look for wrong balances, duplicate accounts, dates that do not match, or debts that do not belong to you.

A dispute should be clear and specific. Do not write a long emotional story. State what is wrong, attach proof, and ask the bureau to investigate. If a medical debt was paid by insurance, include the explanation of benefits or provider statement. If the account belongs to someone with a similar name, say that plainly.

One practical example: a Texas renter applies for an apartment and gets denied because a utility collection appears under the wrong middle initial. A clean dispute with identity documents and old service records can do more than a dozen phone calls. Precision beats outrage.

Why Payment Alone May Not Clean the Damage

Paying a collection does not always remove it from your credit report. That surprises people, and it feels unfair. Payment may update the balance to zero, but the account can still remain for the allowed reporting period if it is accurate.

This does not mean payment has no value. A paid account can look better to some lenders than an unpaid one. It may also stop calls and reduce lawsuit risk. Still, you should understand the credit effect before you hand over money.

Ask whether the collector will report the account as paid, settled, or deleted. Get any promise in writing before sending funds. Verbal promises vanish fast when the next agent answers the phone.

Responding When a Collector Breaks the Rules

Some collectors stay within the law. Others count on the fact that scared people do not take notes. Your best defense is not anger. It is documentation, pattern recognition, and a clear next step.

What to Record When Fair Debt Collection Goes Wrong

Fair debt collection breaks down when a collector threatens, insults, lies, calls too often, contacts the wrong people, or ignores written requests. Your job is to capture the pattern. Keep a log with dates, times, phone numbers, names, and short notes about what was said.

Save letters, voicemails, emails, screenshots, and payment agreements. Do not edit them. Do not rely on memory. A clean record can help a regulator, attorney, or credit bureau understand what happened without turning your story into a guessing game.

A strange thing happens when you start writing everything down. You feel less cornered. The collector may still be loud, but the facts become quieter and stronger.

Where Collection Agency Rules Give You Leverage

Collection agency rules give you options when a collector ignores legal limits. You may send a written request telling the collector to stop contacting you. That does not erase the debt, and it does not prevent a lawsuit, but it can stop the noise.

You can also file complaints with consumer protection agencies or speak with a consumer rights lawyer. Some lawyers review collection abuse cases because federal law may allow fee recovery when collectors violate your rights. That means getting legal help may be more realistic than people assume.

Do not threaten action you are not prepared to take. A steady letter, a well-kept file, and a timely complaint often carry more weight than a furious call. Calm pressure is still pressure.

Building Long-Term Financial Protection After Collection Stress

A collection problem usually reveals a larger weak spot. Maybe mail went unopened. Maybe medical billing was impossible to follow. Maybe a card balance grew during a job gap. Whatever caused the pressure, the next step is to build a system that catches problems earlier.

Why Consumer Debt Protection Starts Before the First Call

Consumer debt protection is not only about reacting to collectors. It starts with opening bills, checking statements, saving notices, and knowing which debts carry the highest risk. A small routine can prevent a large mess.

Set one weekly money check-in. Review mail, email, bank activity, credit alerts, and upcoming due dates. It does not need to feel like a finance meeting. Fifteen focused minutes can catch a billing mistake before it becomes a collection account.

The unexpected insight is that organization often beats income. Plenty of high-earning households fall into collection trouble because paperwork gets ignored. A lower-income household with clean records may have a stronger defense when a collector makes a mistake.

How Credit Report Disputes Fit Into a Yearly Money Routine

Credit report disputes should not be a last-minute move before a mortgage application. Make credit review part of your yearly routine. Look for unfamiliar accounts, wrong balances, old addresses, and collections that reappear under new names.

Keep a folder for resolved debts, settlement letters, payment confirmations, and dispute results. Digital copies are fine, but name the files clearly. “Paid Capital One settlement March 2026” is far more useful than a random screenshot buried in your phone.

Financial protection is not about perfection. It is about being hard to mislead. When your records are organized, collectors have less room to rush you, confuse you, or rewrite the facts.

Conclusion

A collection notice should never make you feel powerless. It should make you pause, gather facts, and respond with control. The strongest move is not always paying fast, arguing loudly, or ignoring the problem. The strongest move is knowing which proof to request, which records to save, and which pressure tactics cross the line.

Your debt collection rights are not abstract legal language. They are practical tools for protecting your paycheck, your credit, your privacy, and your peace of mind. Use them early, use them in writing, and do not let a collector’s urgency become your mistake.

Start by reviewing the last collection letter, checking your credit reports, and creating one folder for every document tied to the account. A clear record turns confusion into leverage, and leverage is where financial protection begins.

Frequently Asked Questions

What should I do first after receiving a debt collection letter?

Read the letter carefully, save the envelope, and avoid paying right away until you understand the claim. Check the creditor name, balance, and deadline for disputing the debt. If anything looks wrong or unfamiliar, send a written request asking for validation.

Can a debt collector call my job in the United States?

A collector may try to contact you at work, but they must stop if you tell them your employer does not allow those calls. They also cannot discuss your debt with your boss or coworkers. Keep notes if workplace contact continues after your request.

How do I know whether a collection debt is real?

Ask the collector to validate the debt in writing. The response should identify the original creditor, the amount claimed, and the collector’s authority to collect. Compare that information with your own records before paying or agreeing to any settlement.

Can debt collectors threaten arrest for unpaid bills?

Collectors generally cannot threaten arrest for ordinary consumer debt. Unpaid credit cards, medical bills, or personal loans are civil matters, not criminal cases. Threats of jail are a serious warning sign, and you should document the call and consider filing a complaint.

Will paying a collection account remove it from my credit report?

Payment does not always remove a collection account. It may update the balance to paid or settled, but the account can remain if it is accurate. Ask for any deletion or reporting agreement in writing before you send money.

What proof should I keep when dealing with collectors?

Save letters, emails, voicemails, screenshots, payment receipts, dispute letters, and delivery confirmations. Keep a call log with dates, times, names, and short notes. Good records make it easier to challenge errors, report abuse, or defend yourself if a lawsuit appears.

Can I tell a debt collector to stop contacting me?

Yes, you can send a written request asking the collector to stop contacting you. This may stop calls and letters, but it does not erase the debt. The collector may still take legal steps, so use this option with a clear plan.

When should I contact a consumer rights attorney?

Contact an attorney if a collector threatens you, sues you, contacts others about your debt, ignores written requests, or reports false information. Legal help is also smart before paying old debt, because state rules can affect lawsuit deadlines and repayment risks.